The Evolution of a Wealth Market: Why South Florida's Next Chapter May Be Its Most Important Yet

For much of the past five years, South Florida has been one of the most closely watched real estate markets in the world.

Population growth accelerated.

Businesses relocated.

Capital flowed in.

Property values appreciated.

What began as a migration trend has gradually evolved into something much larger.

Today, South Florida is no longer simply benefiting from momentum. It is increasingly being recognized as a long-term wealth market.

And that distinction matters.

A Market Entering a More Sophisticated Phase

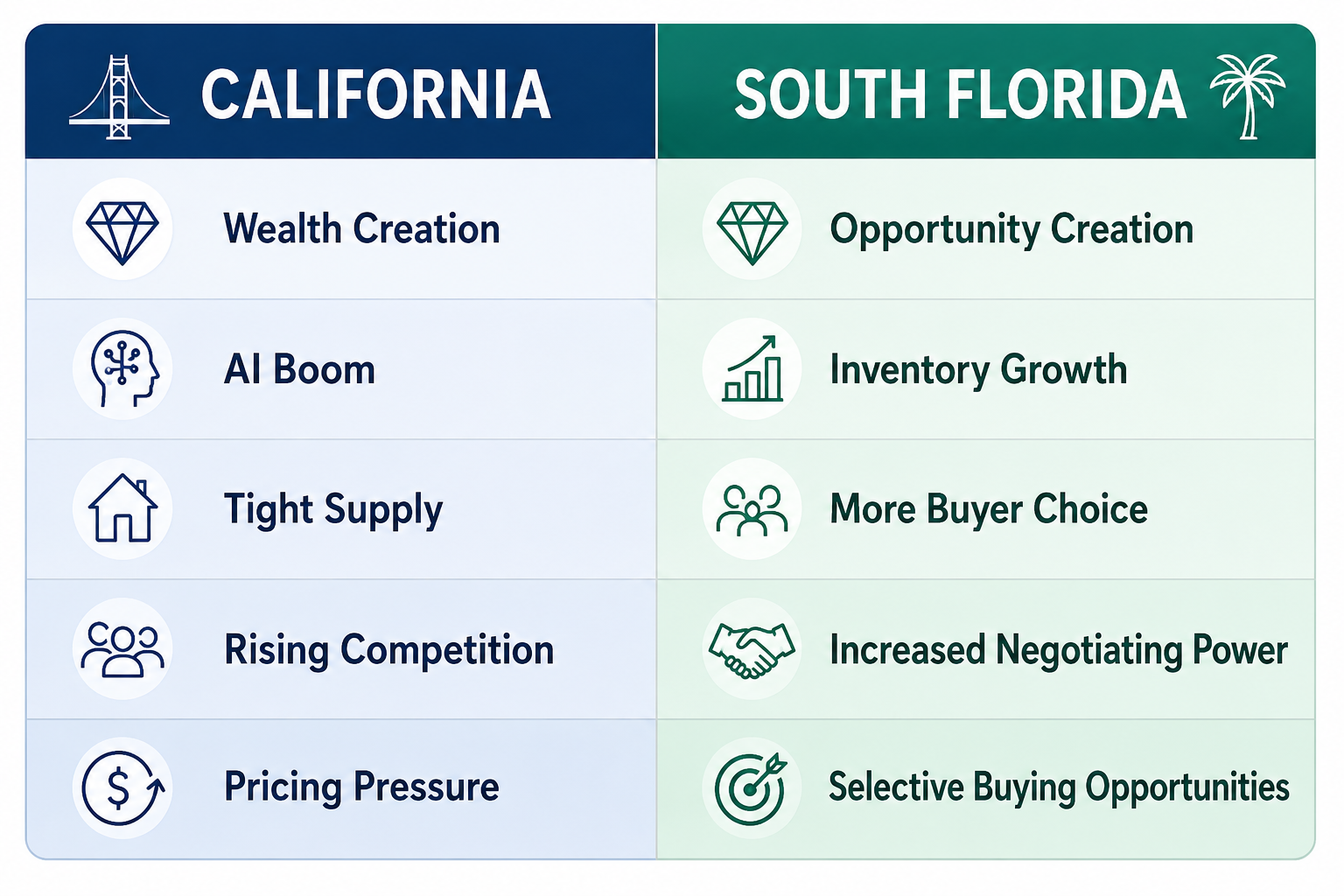

Many observers see rising inventory levels and longer marketing times and assume the market is slowing.

The reality is more nuanced.

Across Miami-Dade, Broward, and Palm Beach Counties, the market is becoming more selective, more disciplined, and arguably healthier.

Buyers have more choices.

Sellers are required to be more strategic.

And transactions are increasingly driven by quality rather than urgency.

This is not the disappearance of demand.

It is the maturation of demand.

The strongest properties continue to attract attention, while assets lacking differentiation face greater competition.

In many ways, South Florida is beginning to resemble other established global wealth markets where location, scarcity, and long-term desirability matter more than short-term market cycles.

Why Capital Continues Moving To South Florida

Perhaps the most important trend remains unchanged.

Capital continues migrating to South Florida.

Entrepreneurs, executives, investors, family offices, professional athletes, and international buyers continue selecting the region for reasons that extend far beyond real estate.

Several factors continue supporting this migration:

- A favorable tax environment

- Global connectivity through major airports and seaports

- Expanding business opportunities

- Strong population growth

- Lifestyle advantages that few destinations can replicate

- Increasing international relevance

For many affluent households, purchasing real estate in South Florida is no longer simply a housing decision.

It is a capital allocation decision.

Real estate has become part of a broader strategy involving wealth preservation, lifestyle optimization, and long-term positioning.

The Rise of Strategic Ownership

The luxury buyer of 2026 is different from the luxury buyer of 2021.

Today's conversations focus less on timing the market and more on identifying enduring value.

Sophisticated buyers are asking:

- Is this location irreplaceable?

- Does this property possess true scarcity?

- How will this asset perform over the next decade?

- Does it align with my family's future lifestyle needs?

- Can it preserve purchasing power over time?

This shift is particularly evident within:

- Waterfront residences

- Branded residences

- Trophy properties

- Luxury condominiums with exceptional amenities

- Walkable urban neighborhoods

- New construction opportunities in supply-constrained locations

These assets continue attracting significant interest because they offer characteristics that cannot easily be replicated.

The Growing Appeal of Branded Residences

One of the most compelling trends shaping South Florida's luxury market is the continued rise of branded residences.

Projects such as Faena Residences Miami, The St. Regis Residences Miami, Cipriani Residences, and Mercedes-Benz Places are redefining how affluent buyers evaluate luxury real estate.

Today's purchasers increasingly seek more than square footage and views.

They seek:

- Service

- Privacy

- Wellness

- Security

- Design excellence

- Lifestyle integration

Branded residences provide a level of consistency and global recognition that resonates strongly with both domestic and international buyers.

As a result, this segment continues to command significant attention and pricing power.

The Importance of Scarcity

As markets mature, scarcity becomes increasingly valuable.

This is especially true within South Florida.

Whether it is a waterfront estate on the Venetian Islands, a trophy residence in Coconut Grove, or a limited collection penthouse within a branded development, buyers are placing greater emphasis on assets that cannot easily be duplicated.

Scarcity often creates resilience.

And resilience is precisely what sophisticated investors seek during periods of market transition.

While broader inventory levels may fluctuate, truly exceptional properties frequently operate under different market dynamics.

Looking Ahead

The next phase of South Florida's evolution may prove to be its most important.

The region continues attracting global talent, investment capital, entrepreneurs, and full-time residents.

Infrastructure investment continues.

Business migration continues.

International demand continues.

Most importantly, the market is developing the characteristics commonly associated with established global wealth centers.

For investors, homeowners, and families alike, the opportunity may no longer be about chasing appreciation.

Instead, it may be about securing a position within one of the world's most dynamic and desirable markets before the next chapter fully unfolds.

Final Thought

Great markets evolve.

South Florida is doing exactly that.

The conversation is no longer solely about growth.

It is increasingly about permanence.

And for those taking a long-term view, that may represent the most compelling opportunity of all.