Foreclosures are rising as taxes, insurance, HOA dues, and ownership costs squeeze homeowners. Why today’s affordability crisis goes far beyond mortgage rates.

The Hidden Affordability Crisis: Why It’s No Longer Just About Mortgage Rates

For the past two years, housing affordability has been discussed almost entirely through one variable:

mortgage rates.

Would rates fall?

Would payments improve?

Would buyers return?

But that focus is now incomplete.

A major national housing report released this week showed U.S. foreclosure filings rising nearly 26% year-over-year in Q1, reaching the highest level in six years.

Not because of reckless lending.

Not because of adjustable mortgages resetting.

But because the total cost of owning a home is climbing faster than many homeowners expected.

This is creating a hidden affordability crisis.

❝ Today’s affordability pressure is no longer just loan-related — it is ownership-cost related. ❞

The Monthly Payment Is No Longer Just the Mortgage

For years, buyers used a simple formula:

Purchase Price + Interest Rate = Monthly Payment

Today, that no longer tells the full story.

Homeownership now carries a growing list of expenses beyond principal and interest:

- property taxes,

- homeowners insurance,

- HOA and condo dues,

- reserve assessments,

- maintenance and utility inflation.

Many owners still have fixed mortgages they can afford.

What is straining them is everything surrounding the mortgage.

That is the shift this recent foreclosure data is signaling.

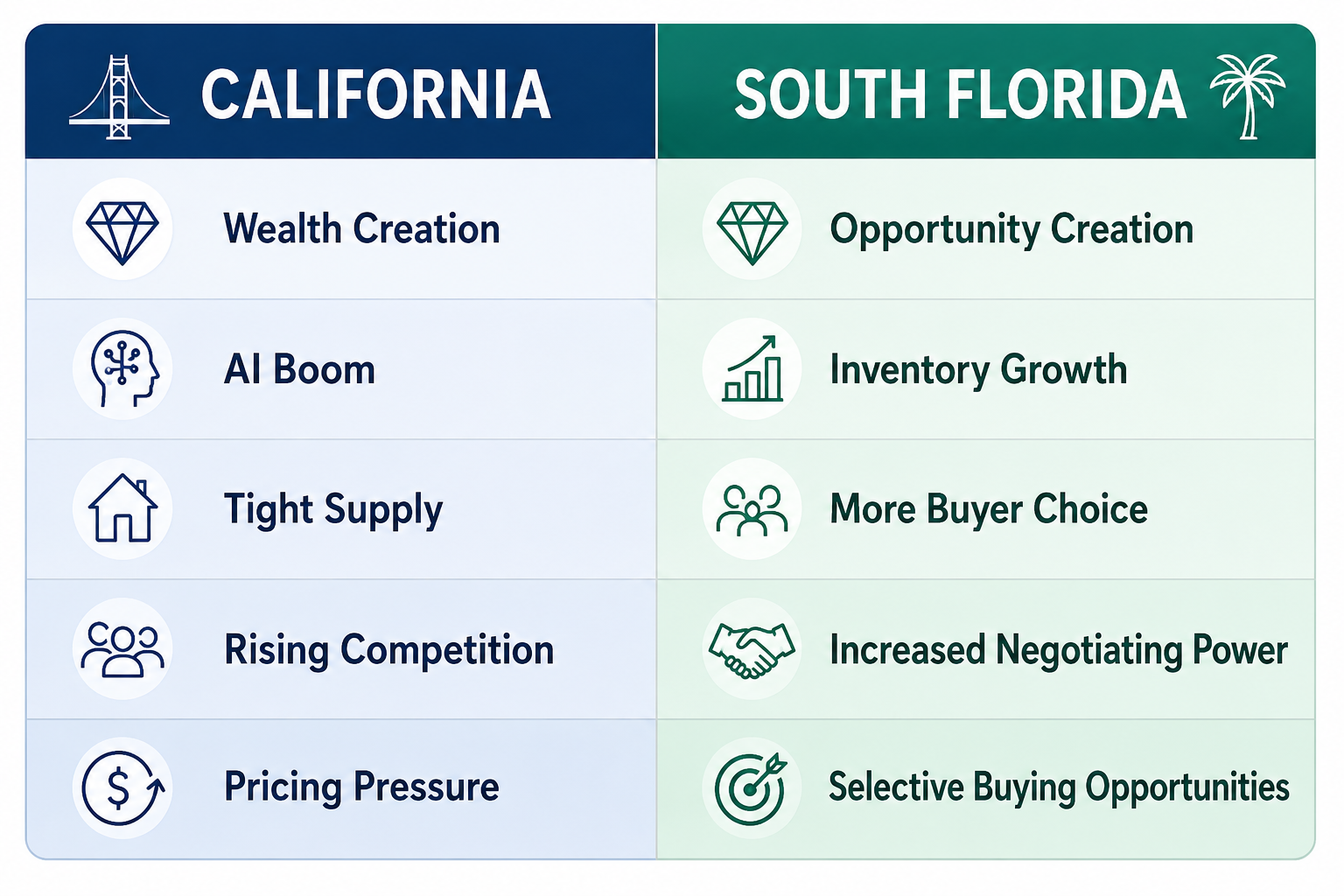

Why This Matters in California and Florida

As I advise buyers across both California and Florida, I am seeing the same pattern emerge in different forms.

Florida

Buyers today face:

- sharply rising insurance premiums,

- HOA reserve increases,

- condo special assessments,

- deferred maintenance catch-up.

The purchase price may still look attractive.

The all-in monthly carry often does not.

Florida ranked among the states with the heaviest foreclosure pressure in Q1 as ownership costs continue to climb.

California

California’s issue is cumulative ownership burden:

- high property tax carry,

- insurance repricing,

- elevated utility costs,

- maintenance inflation.

Because acquisition prices are already high, there is less room for secondary expenses to rise without creating monthly strain.

Different market.

Same affordability compression.

❝ In many cases, the lower-priced property is no longer the lower monthly burden. ❞

The Dangerous Assumption Buyers Still Make

Many buyers still believe:

“If I qualify for the mortgage, I can afford the home.”

That is no longer enough.

Mortgage approval does not automatically mean:

- the insurance burden is sustainable,

- the HOA is healthy,

- the tax profile is manageable,

- or the long-term carrying costs are comfortable.

Lender approval and ownership safety are no longer the same thing.

What Smart Buyers Are Doing Differently in 2026

The smartest buyers are no longer asking only:

“What rate can I get?”

They are asking:

“What is the all-in monthly cost of controlling this asset?”

That means evaluating:

- property tax trajectory,

- insurance exposure,

- HOA financial health,

- pending assessments,

- long-term monthly carry.

Because increasingly:

- the lower-priced property is not the lower monthly burden,

- and the lower mortgage rate is not the complete affordability answer.

The property now needs to be underwritten as carefully as the financing.

❝ In 2026, mortgage approval does not automatically equal payment safety. ❞

The housing market’s affordability issue has evolved.

It is no longer just about mortgage rates.

It is about whether the total financial instrument of ownership still works once taxes, insurance, HOA obligations, and carrying costs are layered in.

That is where today’s hidden payment shock is occurring.

And that is where smarter buyers can still protect themselves—by analyzing the financing and the asset together.

Need a Full Ownership-Cost Review Before Buying?

If you are considering a purchase in California or Florida, I’m happy to provide a full all-in affordability review before you write an offer.