If you’ve been watching mortgage rates closely, you may have noticed something subtle—but powerful—happening. Mortgage rates just declined for the second straight week, and for investors **investing in Miami**, this shift is quietly reopening doors that were firmly shut just a year ago.

According to Freddie Mac as of December 4:

30-Year Fixed: 6.19% (down 50 basis points year-over-year)

15-Year Fixed: 5.44% (down 52 basis points year-over-year)

This isn’t headline-grabbing news. But for high-net-worth buyers pursuing **Miami condominiums**, luxury second homes, and full-service residences, this environment creates leverage—if you know how to use it. In this guide, I’ll show you exactly what’s changing, why it matters, and how smart buyers are positioning themselves right now.

1. Why Mortgage Rates Are Drifting Lower Right Now

Mortgage rates don’t move solely based on headlines—they respond to deeper macroeconomic forces.

Here’s what’s driving today’s shift:

The Federal Reserve, through the Federal Open Market Committee, has cut interest rates twice in 2025

A strong probability exists for one more cut in December

Mortgage rates closely follow the 10-Year Treasury yield, which is now lower than this time last year

Lender spreads have tightened, improving consumer pricing

While the Fed doesn’t directly control mortgage rates, lenders anticipate policy moves—and that’s exactly what’s unfolding now. Today’s rates are meaningfully better than 12 months ago, even if we’re not yet at 6.00%.

For those **investing in Miami**, this creates a strategic window before the broader market reacts.

2. The Biggest Myth Buyers Still Believe About Rates

Here’s the uncomfortable truth most headlines miss:

**Waiting for the “perfect” rate is often the most expensive strategy.**

Why?

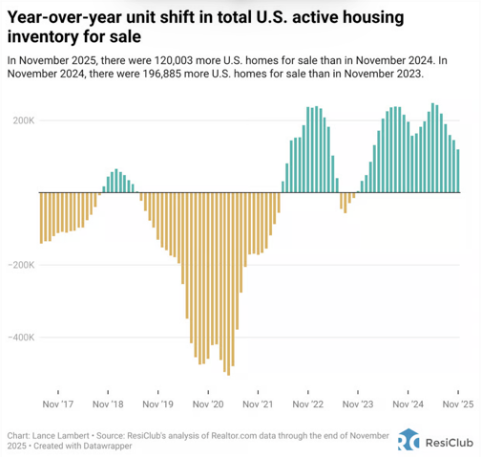

Housing supply remains tight

Buyer demand has not disappeared

Home prices continue climbing in prime Miami markets

When rates fall quickly, competition surges overnight

I see this cycle repeatedly with second-home buyers. Many wait for confirmation. Then when rates dip aggressively, bidding wars return, inventory vanishes, and pricing accelerates—erasing the savings buyers hoped to gain from lower interest.

Speed beats speculation in luxury real estate.

3. What Smart Buyers Are Doing Instead of Waiting

The most sophisticated buyers aren’t waiting for perfect conditions—they’re engineering leverage now.

Here’s what my high-net-worth clients are doing today:

1. Buying smaller or smarter rather than delaying

2. Using renovation financing to reposition assets

3. Targeting value within prime **Miami condominiums**

4. Leveraging temporary and permanent rate buydowns

5. Considering 15-year mortgages to accelerate long-term wealth

6. Expanding search zones for better value per square foot

This is where deep local intelligence matters. Many luxury buyers don’t have time to research zoning changes, HOA structures, reserve studies, or building financials. They want to be spoon-fed certainty—and that’s exactly what strategic guidance offers.

4. Why Investing in Miami Still Dominates Secondary Home Strategy

For high-net-worth individuals, **investing in Miami** isn’t just about appreciation—it’s about lifestyle integration, asset protection, and global flexibility.

Miami offers something few global cities can simultaneously deliver:

Luxury waterfront real estate

Full-service property management

Strong international buyer demand

Favorable tax structure

Year-round rental liquidity

World-class dining, entertainment, and culture

For clients who already own property in New York, California, London, São Paulo, or Toronto, Miami acts as both:

A lifestyle anchor for family time, vacations, and seasonal living

A capital preservation asset with upside

That combination is rare—and it’s exactly why demand remains resilient even when rates rise.

5. Why Luxury Condominium Buyers Hold the Advantage Right Now

Today’s market heavily favors buyers who prioritize **luxury condominium** living with:

Full-service amenities

24-hour security and doorman

Concierge services

Valet parking and dedicated **parking**

Resort-style pools, spas, and wellness centers

For wealthy buyers who don’t want to manage property, deal with vendors, or worry about maintenance, condo living delivers simplicity at scale.

And right now, the resale condo market presents a rare alignment:

Some motivated sellers

Improved mortgage pricing

Strategic negotiation leverage

Less competition than peak frenzy periods

This is the exact environment where disciplined buyers quietly build extraordinary long-term positions.

6. What the Big Forecasts Say About the Road Ahead

Industry projections confirm that today’s conditions are transitional—not permanent.

Mortgage Bankers Association projects 30-year rates around 6.4% through 2026

Fannie Mae expects rates could reach approximately 5.9% by late 2026

This means today’s buyers are positioning themselves **before** the next major demand surge—not chasing it after the fact. Historically, the largest wealth transfers in real estate occur in these transition windows.

7. PRO-TIP: Strategy Beats Rate Every Time

You don’t need perfect rates to win—you need the **right strategy for today’s market**.

That means:

Buying before competition returns

Structuring flexible financing

Selecting buildings with strong reserves and elite management

Positioning for future appreciation, not short-term headlines

This is especially critical for buyers seeking **new development**, premium **amenities**, enhanced **security**, and turn-key living.

8. Where to Find the Best Miami Buildings Right Now

If your priority is simplicity, security, and full-service living, start with curated access to Miami’s most elite towers and communities.

You can explore vetted developments and luxury buildings here:

https://www.chrispessymiamirealestate.com/buildings

This resource allows buyers to quickly compare:

Building features

Amenities

Security profiles

Lifestyle offerings

Location advantages

For non-local buyers, this shortens research time dramatically.

9. A Simple Scenario I See Every Week

A client from the Northeast recently reached out after waiting 14 months for rates to drop under 6%. During that time, the exact Miami residence they loved appreciated over $480,000. Their monthly payment today—**even with slightly higher rates**—is still higher than if they had acted earlier.

Meanwhile, buyers who moved decisively twelve months ago are sitting on:

Locked pricing

Lower basis

Rental income

Equity already created

The lesson is simple: waiting for certainty often costs more than acting with strategy.

Conclusion: The Window Is Quiet—But It’s Open

Mortgage rates drifting lower for the second straight week may not dominate headlines—but for buyers **investing in Miami**, it changes the playing field dramatically.

Luxury demand remains strong. Inventory remains tight. And when rates drop meaningfully again, buyer competition will accelerate fast.

If your goal is:

A turnkey second residence

Zero maintenance ownership

Full-service living with elite amenities

Security, simplicity, and lifestyle integration

Then this market rewards strategic action—not hesitation.

FAQs

1. Is now a good time for investing in Miami condos?

Yes. Today’s combination of softened competition, improved rates, and motivated sellers creates an ideal entry window for long-term buyers.

2. Are luxury condominiums safer than single-family homes?

For many second-home buyers, yes. Condos provide managed maintenance, enhanced security, and full-service living without operational burdens.

3. Will rates continue falling in 2025?

Forecasts suggest stabilization near current levels with gradual improvement into late 2026, not sudden drops.

4. Why do wealthy buyers prefer full-service buildings?

They value time, simplicity, security, concierge services, and the ability to “lock and leave” without worrying about property management.

.avif)

.jpg)

.jpg)