Inflation reached 4.2% in May, but core inflation remained contained. Here's what it means for mortgage rates, homebuyers, and investors.

Inflation Hits 4.2%: Why the Headline Doesn't Tell the Full Story for Homebuyers

At first glance, last week's inflation report appeared to deliver another setback for prospective homebuyers.

The Consumer Price Index (CPI) rose 4.2% year-over-year in May, marking its highest annual reading in nearly three years. Since inflation plays a major role in interest rate decisions, many immediately assumed mortgage rates would remain elevated for the foreseeable future.

However, the underlying data tells a more nuanced story—one that may be more encouraging for both buyers and real estate investors.

Looking Beyond the Headline

Inflation headlines often focus on the overall CPI figure, but economists frequently look deeper to understand what's truly happening within the economy.

A significant portion of May's inflation increase was driven by rising energy costs. Gasoline, transportation, and energy-related expenses experienced noticeable increases, pushing the headline inflation number higher.

When those more volatile categories are removed, the picture changes considerably.

Core inflation—which excludes food and energy prices—rose just 2.9% year-over-year.

This distinction is important because core inflation is one of the Federal Reserve's preferred measures when evaluating longer-term inflation trends.

According to several economists, core inflation continues moving closer to the Federal Reserve's long-term target of approximately 2%, suggesting that broader inflationary pressures remain relatively contained.

Why This Matters for Mortgage Rates

Mortgage rates are influenced by many factors, but inflation remains one of the most significant.

When inflation rises rapidly, investors typically demand higher yields on bonds, including mortgage-backed securities. Those higher yields often translate into higher mortgage rates for consumers.

The latest inflation report is unlikely to trigger immediate mortgage rate relief. Most analysts expect the Federal Reserve to remain cautious as it evaluates incoming economic data.

However, the report also does not suggest that inflation is accelerating uncontrollably throughout the economy.

Instead, it reinforces the narrative that inflation remains a challenge, but one that appears increasingly concentrated in specific sectors rather than broadly across all goods and services.

For homebuyers, that distinction matters.

The Housing Market Remains in a Holding Pattern

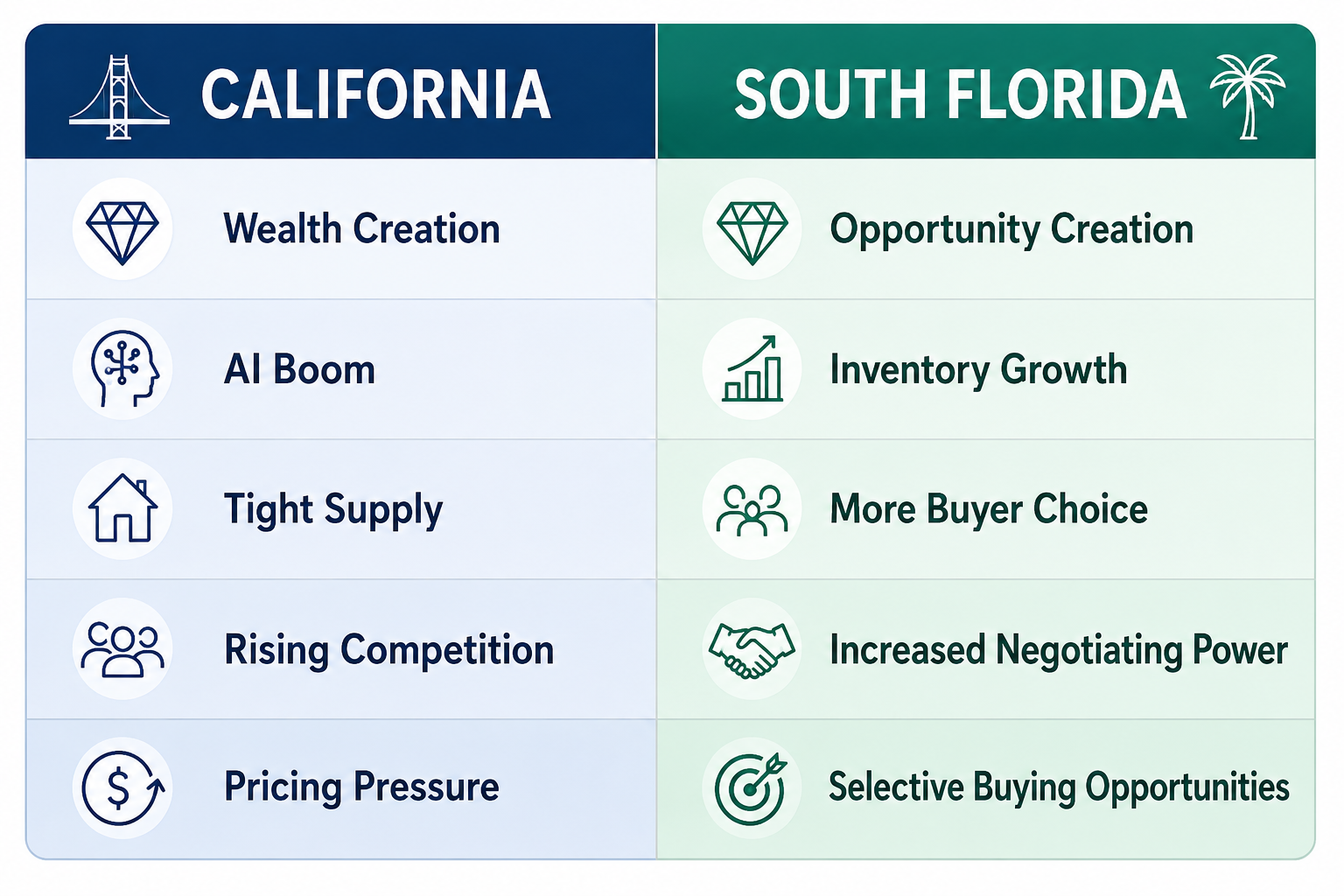

Across many markets—including California and South Florida—buyer demand has not disappeared.

Rather, much of the demand appears to be waiting.

Potential buyers continue monitoring mortgage rates while evaluating affordability and market conditions. At the same time, inventory levels have improved compared to the extremely constrained conditions experienced over the past several years.

This combination has created a more balanced environment than many buyers have seen in quite some time.

Today's market offers:

- More inventory options

- Greater negotiating leverage

- Reduced competition compared to peak pandemic years

- Opportunities for long-term investors focused on fundamentals

While some buyers continue waiting for lower rates, others are taking advantage of improved market conditions before broader demand returns.

A Tale of Two Markets

One interesting dynamic emerging in today's housing market is the growing divergence between luxury and traditional housing segments.

In many luxury markets, particularly in South Florida, affluent buyers remain active despite elevated borrowing costs. Cash buyers continue to represent a significant share of transactions, helping support demand for premium properties.

Meanwhile, many traditional buyers remain more sensitive to financing costs and are watching the Federal Reserve closely for signs of future rate reductions.

This creates unique opportunities depending on a buyer's objectives, financial profile, and investment horizon.

What to Watch Next

The Federal Reserve's upcoming meetings will remain a major focus for financial markets.

While most economists expect policymakers to keep benchmark rates unchanged in the near term, future inflation reports will help determine whether rate cuts become more likely later this year.

Investors and homebuyers should pay particular attention to:

- Future core inflation readings

- Employment data

- Consumer spending trends

- Federal Reserve commentary

- Treasury bond market movements

These indicators will likely provide a clearer picture of where mortgage rates may head over the coming months.

Final Thoughts

The 4.2% inflation headline captured attention, but the underlying data tells a more balanced story.

While inflation remains above the Federal Reserve's long-term target, much of May's increase was driven by energy costs rather than widespread price acceleration throughout the economy.

For buyers, sellers, and investors, the current environment continues to present opportunities—particularly for those focused on long-term wealth creation rather than short-term market headlines.

Markets rarely reward those who wait for perfect conditions.

More often, opportunities emerge when uncertainty creates hesitation among the broader market.

As always, understanding the difference between headlines and underlying trends remains one of the most valuable advantages any investor can have.